AXTI: Extreme IV in a Heavy Put Structure

Options volatility near 166% with a Gamma Wall tilted toward puts and key levels clustered around 77, 79, and 90.

AXTI currently sits in one of the more extreme volatility regimes on the board. Options are pricing implied volatility around 166%, which means the market expects very large potential moves over a short horizon. In practical terms, that tells us traders are paying a high price for both protection and leverage, often because past swings have been sharp and news flow has been uncertain. For self-directed traders, this matters because option prices are sensitive not just to direction, but to how much the stock can move in either direction.

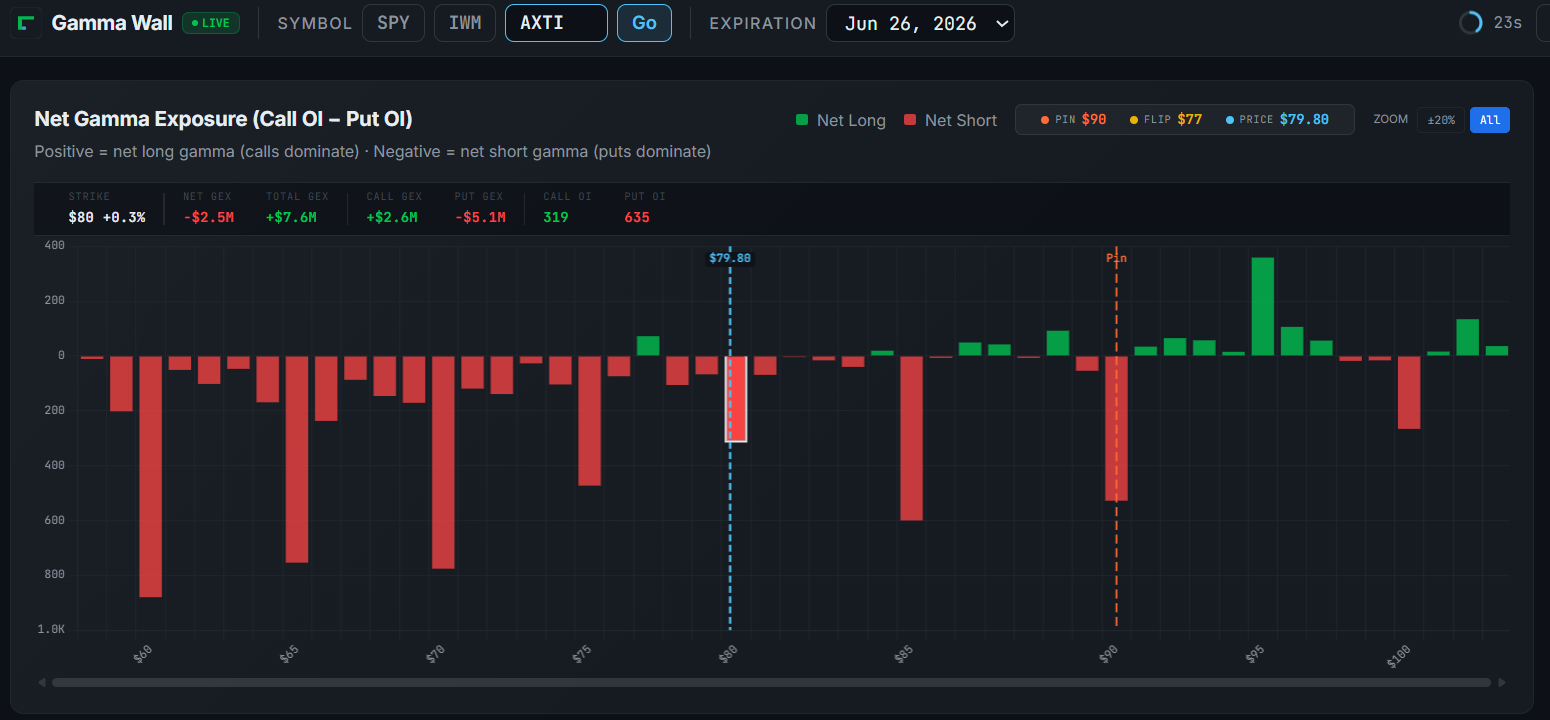

The Gamma Wall snapshot adds important context. Most strikes show net short gamma, with large red bars where put open interest dominates and fewer green bars where calls provide counterweight. The current price is marked near 79, below the gamma pin level around 90 and close to the gamma flip near 77. On the right side of the panel, put open interest stacks up at 60, 65, and 70, forming a ladder of potential support where many traders and hedgers are already active. Call walls are higher, at 90, 95, and 100, suggesting upside resistance where call exposure grows.

This mix — very high implied volatility and a gamma profile tilted toward puts — means dealers are more likely to hedge in the direction of a strong move instead of calming it. If AXTI breaks lower, hedging can add selling; if it squeezes higher through key strikes, the same mechanics can add buying.

From here, I would watch three things closely: how AXTI trades around the gamma flip near 77, whether price tests the heavy put areas below 70, and whether implied volatility starts to cool off or stays elevated after any move. Likely scenarios are a choppy range where IV slowly bleeds as levels hold, or a sharper trend where IV proves justified and the stock follows through more than usual. The cleanest invalidation for any short-volatility or tight-range idea is a break of support with IV staying high and volume increasing, not falling.

For a clearer view of how these call and put exposures change over time and where gamma is most concentrated, the Net Gamma Exposure view inside QNTR Tools is the right place to start.

Short at-the-money straddle with delta hedging (concept)

Goal: Sell both an at-the-money call and put, then use the stock itself to smooth out directional risk as price moves.

Example structure:

Expiration: July 17

Sell one at-the-money call

Sell one at-the-money put

This takes in premium but is exposed if AXTI moves strongly up or down. To manage that directional risk, traders can “delta hedge.” In plain terms, that means:

- If AXTI moves up, the position becomes more sensitive to further gains. You can sell some shares to push the overall position back toward neutral.

- If AXTI moves down, you can buy some shares to balance the growing downside sensitivity.

Delta hedging does not remove risk. It spreads risk between options and stock and attempts to keep the position from becoming too one-sided. In a name with IV near 166%, the main caveats are trading costs from frequent hedge adjustments, gaps where the stock moves before you can react, and the possibility that AXTI trends hard enough that both the short options and the stock trades become uncomfortable. Clear rules about how much stock to trade and when to close the position matter as much as the initial setup.