Warsh’s Hawkish Debut: No Cuts, One Possible Hike, and a Fed Rewired from the Inside

Kevin Warsh’s first FOMC meeting delivered a unanimous hold but a major break from Powell-era communication — stripped forward guidance, an inflation upgrade, a raised dot plot, and five new task forces restructuring how the Fed operates. Here’s what it means for rates, the dollar, metals, and equities.

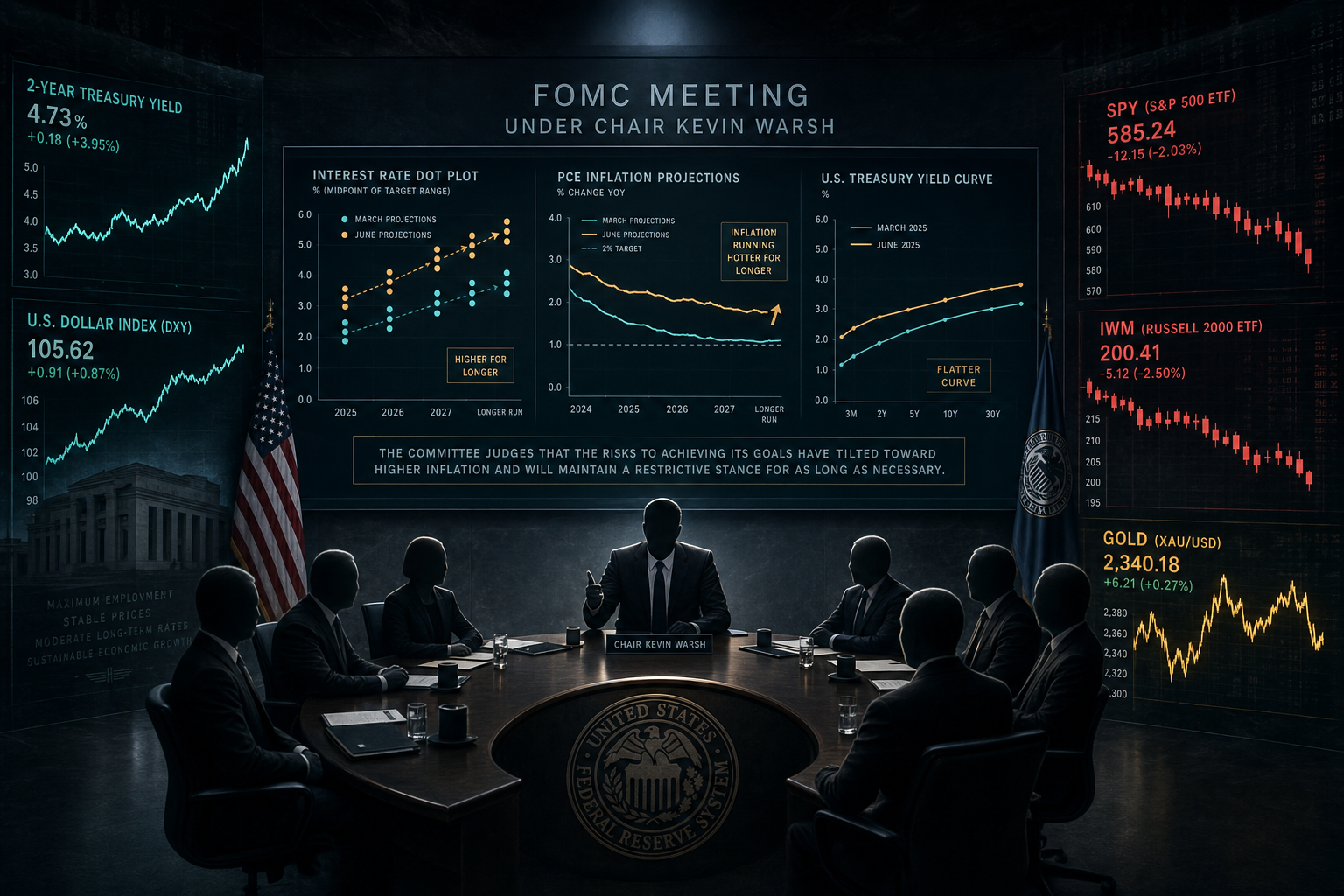

The Main Takeaways

- The Fed held rates at 3.50%–3.75%, but the hold itself was not the story.

- The updated SEP was hawkish: inflation forecasts moved higher and the median policy path shifted from one cut previously to a possible hike.

- Warsh removed forward guidance and even withheld his own dot, signaling discomfort with the Fed’s prior communications framework.

- Five new task forces suggest this was not just a policy meeting but the start of a structural overhaul inside the Fed.

- Markets heard “higher for longer”: front-end yields rose, the dollar strengthened, gold sold off initially, and equities — especially rate-sensitive areas — came under pressure.

The market was prepared for a hold. It was not fully prepared for a Fed chair willing to abandon the easing narrative, question the dot plot, and launch broad internal reviews that could reshape how policy is communicated going forward.

The Hawkish Tone

Warsh’s tone was hawkish less because he explicitly promised hikes and more because he refused to give markets the reassurance they had become used to. The statement was shortened dramatically, the easing bias disappeared, and the press conference leaned into uncertainty rather than policy path management.

In practical terms, that means the Fed is no longer trying to cushion markets with carefully staged language. Instead, it is signaling that inflation remains the primary concern, that rate cuts are off the table for now, and that additional tightening remains possible if incoming data fails to improve.

This was a hold in name, but functionally it was a hawkish repricing event.

Updated SEP: What Changed

The Summary of Economic Projections delivered the clearest message. Inflation forecasts moved up meaningfully, while growth and labor-market projections did not deteriorate enough to justify easier policy. That combination is what gives the June SEP its hawkish edge.

| Metric | Prior | Updated | Read |

|---|---|---|---|

| 2026 Headline PCE | 2.7% | 3.6% | Inflation revised sharply higher |

| 2026 Core PCE | 2.7% | 3.3% | Core inflation now more persistent |

| 2026 GDP | 2.4% | 2.2% | Softer, but not recessionary |

| 2026 Unemployment | 4.4% | 4.3% | Labor market still stable |

| Median Fed Path | One cut bias | Possible hike bias | Clear higher-for-longer message |

The most important macro conclusion is simple: the Fed now sees inflation as more persistent than it did just one quarter ago, while still viewing the broader economy as resilient enough to tolerate restrictive policy.

Warsh’s Task Forces

The task forces may end up mattering as much as the SEP. They suggest Warsh is not just adjusting rates; he is reassessing the institutional machinery behind how the Fed thinks, communicates, and executes policy.

A review of forward guidance, SEP usage, the dot plot, and how the Fed talks to markets. This is the clearest sign Warsh believes prior communication tools may have become too influential or too rigid.

A review of the Fed’s $6.7 trillion balance sheet and the role of quantitative policy in overall financial conditions. This matters for liquidity, term premium, and long-end Treasury behavior.

A review of how the Fed gathers and interprets macro data, including whether it should rely less on lagging indicators and more on broader or faster inputs.

A review of labor-market structure and productivity trends, which may influence how the Fed interprets maximum employment and the economy’s non-inflationary speed limit.

A deeper review of inflation drivers and possibly even the framework used to pursue price stability. This is the most consequential long-term task force because it could reshape how the Fed defines success.

In plain English, the market should assume that the Fed under Warsh may become less transparent, less attached to legacy policy frameworks, and more willing to tolerate market discomfort in service of inflation control.

What It Means for Financial Markets

Short-Term Rates

Short-term yields should remain the most directly exposed to incoming inflation data. If CPI and PCE stay sticky, the front end can keep repricing higher because the market now has to consider another hike rather than a cut. That makes the 2-year especially sensitive.

Long-Term Rates

Long-term yields may rise more slowly than the front end, which creates a bear-flattening bias. The 10-year has to balance tighter Fed policy against slower growth, fiscal supply, and demand for duration during risk-off episodes. The result is not necessarily a straight-line breakout higher, but rather a persistently elevated range.

The Dollar

A more hawkish Fed supports the dollar through rate differentials. That matters globally: tighter dollar liquidity is a headwind for risk assets, a burden for dollar-funded borrowers, and a pressure point for emerging markets and commodities.

Gold and Metals

Gold’s first reaction was lower because higher real yields and a stronger dollar are immediate headwinds. But the bigger picture is more balanced: geopolitical stress and reserve diversification still support longer-term demand. That means the post-FOMC move looked more like a hawkish shock repricing than a clean long-term breakdown.

SPY

For SPY, the issue is valuation. A higher-for-longer Fed raises discount rates and pressures multiples, especially in the large-cap growth cohort. If earnings remain stable, the downside may come more from multiple compression than from a collapse in fundamentals.

IWM

IWM is more vulnerable than SPY if short rates stay elevated. Small-cap balance sheets are more interest-rate sensitive, refinancing conditions are tighter, and the earlier small-cap recovery thesis depended in part on easier policy arriving. This meeting challenged that assumption directly.

The June meeting does not guarantee another hike, but it does force markets to price a much wider distribution of outcomes. That alone is enough to keep rates volatility elevated and to challenge richly valued risk assets.

What Traders Should Watch Next

- Core inflation prints: If core PCE and CPI keep running hot, the hike narrative strengthens.

- Labor market deterioration: A real weakening in jobs data is the clearest reason the Fed would step back from this hawkish stance.

- Dollar follow-through: A sustained DXY move higher would reinforce the tightening of financial conditions.

- Gold’s reaction to real yields: If gold stabilizes despite higher yields, that says something important about geopolitical and reserve demand.

- Small-cap relative performance: IWM vs. SPY is a clean expression of whether the market still believes in an eventual soft-landing-with-cuts path.

Final Read

Yesterday’s FOMC meeting was not just about holding rates steady. It was about redefining the reaction function. The SEP became more hawkish, the communication style became more opaque, and the institutional review process made clear that Warsh intends to leave a structural mark on the Fed.

For markets, that means fewer assumptions about imminent easing, more sensitivity to inflation data, and a higher probability that volatility remains elevated across rates, FX, metals, and equities. In that environment, front-end yields, the dollar, and small-cap relative weakness deserve close attention.

Disclaimer: This material is for informational and educational purposes only and is not investment advice. Options and securities trading involve substantial risk and may not be suitable for all investors.